Overview

A model risk management framework (MRM) is the structured set of board-approved policies that controls and governs how financial institutions develop, validate, deploy, monitor, and retire every model used in credit, fraud, or compliance decisions. Financial institutions are using AI systems for lending, anomaly detection, underwriting, and customer engagement. To ensure that the outputs remain accurate, unbiased, and auditable throughout, the MRM framework ensures that these AI systems meet the same standards of accountability as traditional credit and risk models.

Key Insights

Model risk management was originally built to govern a handful of credit scorecards, but today, when an average Indian bank runs dozens of AI models, it is reaching an inflection point. The cost of getting it wrong is measured in regulatory penalties and biased lending outcomes that damage customer trust and reputational exposure.

The industry reports show that only 44% of banks properly validate their AI models; meanwhile, 92% of global banks reported active AI deployments in at least one core banking function. The numbers clearly show that deployment is outpacing the governance. The RBI’s FREE-AI Framework, released in August 2025, makes model risk management a board-level obligation. Globally, the April 2026 US interagency guidance replacing SR 11-7 signals the same directional shift.

The blog covers what a complete AI model governance framework looks like in 2026, what it covers and why it is the need of the hour for financial institutions.

What is Model Risk?

Model risk is the potential for financial loss, regulatory penalty, or reputational harm arising from a model’s incorrect, biased or misused outputs.

Model risk can emerge from:

- poor data quality

- flawed assumptions and methodology

- inadequate model monitoring and drift

- poor model implementation

- improper model usage

Of these, data quality is frequently the root cause, which is why a strong data management framework is often the first line of defense against model risk, not an afterthought to it.

What is Model Risk Management?

Model risk management (MRM) is an iterative and structured approach to identifying, assessing, mitigating, and monitoring the risks associated with the models used for credit underwriting, fraud, or compliance decisions.

It ensures that the models are developed, implemented, and used in a controlled and auditable manner for better decision-making processes. It is applied to banks, NBFCs, insurers, fintech lenders and payment system providers.

With the global AI-focused model risk management solutions expected to grow at more than 12% annually through the end of the decade, RBI’s guidelines for regulated entities to govern the entire model lifecycle, from development and selection through deployment, monitoring and periodic revalidation, are a step in that direction.

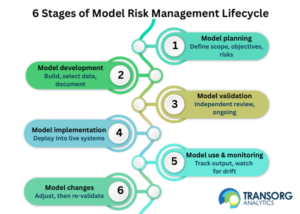

Model Risk Management Framework: The 4 Governance Layers

The below framework defines the 4 governance layers that must be kept in mind by enterprises based on their scope and practical relevance.

- Model Definition and Risk Tiering: Model risk tiering is a structured approach to identifying and ranking models by their potential impact. To allocate validation resources efficiently, the mechanisms classify credit decisioning, fraud detection, and underwriting models as high-risk models and FAQ chatbots and internal reporting dashboards as low-risk models. Without this mechanism, governance effort may be either too thin or concentrated on the wrong models.

- Governance and Oversight: Governance and oversight is the board-approved policy structure that assigns accountability for model risk management, including a model risk committee with authority over approval, exceptions and escalation. Per the RBI’s FREE-AI Framework, its own survey of regulated entities found that board-level AI governance structures and accountability frameworks remain markedly scarce, which is why a detailed board-approved MRM policy is a must for institutions.

- Development and Documentation: Model development and documentation are the requirements that every model, whether internally built or third-party, be documented with its objectives, assumptions, limitations and data sources before deployment for all the stakeholders. RBI guidelines place the accountability for the model on the institution regardless of who built the model. For example, if a bank buys a credit scoring API from a vendor, it owns the validation obligation.

- Independent Validation and Monitoring: Independent ML model validation and audit is an assessment conducted by a team not involved in developing or selecting the model. For adequate model risk management, RBI requires periodic validation with documented escalations before the model and after deployment so that the model outputs are consistent, unbiased, explainable and verifiable. Industry reports suggest that fewer than 15% of RBI-regulated entities currently conduct post-deployment monitoring for bias or performance drift, which is below the standard the RBI’s FREE-AI framework expects.

What is AI Model Governance?

AI model governance is the extension of traditional MRM principles, including tiering, validation, explainability, and monitoring, to machine learning and generative AI systems making consequential decisions.

As institutions increasingly turn to agentic AI and workflow automation to handle these processes end to end, governance becomes inseparable from the automation strategy itself.

Model Risk Management: Explainability and Audit Trails for Banks and NBFCs

A model risk management framework without explainable AI and an audit trail cannot be enforced. For regulators, AI model explainability requirements are evidence that decisions can be understood, reviewed, challenged, and justified.

RBI’s FREE-AI framework highlights the importance of explainability mechanisms such as:

- SHAP (SHapley Additive exPlanations)

- LIME (Local Interpretable Model-agnostic Explanations)

These tools help institutions interpret AI-generated decisions and demonstrate accountability and explain to customers why their loan application was declined.

Beyond the technical method, a defensible audit trail in model risk management has five components:

- Input data lineage

- Model version used

- Decision rationale or feature contribution

- Human override log

- Timestamp and approver record

Model Risk Management Policy: What RBI and Global Regulators Require

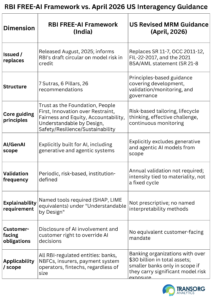

- RBI’s draft circular on Regulatory Principles for Management of Model Risks in Credit is expected to require a board-approved MRM policy covering governance, development, validation, and monitoring across the full model lifecycle.

- RBI’s FREE-AI Framework is built on 7 Sutras and 26 recommendations. The seven core principles, including Trust is the Foundation; People First; Innovation over Restraint; Fairness and Equity; Accountability; Understandable by Design; and Safety/Resilience/Sustainability, underpin recommendations across six pillars, including governance, risk management, model lifecycle management, stakeholder management, innovation enablement, and data stewardship. These extend model risk management, transparency and cybersecurity requirements explicitly to AI systems.

- The April 2026 US Interagency Guidance replacing SR 11-7, OCC 2011-12, and FIL-22-2017 emphasizes risk-based tiering, lifecycle governance, and continuous monitoring. It aligns directionally with RBI’s approach on lifecycle thinking but differs in two important ways: it explicitly excludes generative and agentic AI models from scope, and it applies only to banking organizations with more than $30 billion in total assets.

With these policies being drafted, regulators are signaling that AI models are now central to how banks make decisions and that model risk must be governed with the same rigor as credit or market risk.

5-Question Model Governance Checklist Before Deployment

Before any model goes live in a credit, fraud, or compliance context, the following five questions must be answered with proper documentation for appropriate model risk management:

- Has the model been assigned a risk tier reflecting its materiality and potential impact?

- Is the explainability method well documented and reviewable?

- Has the independent validation been completed by a team not involved in development?

- Does the model have an audit trail AI decisions mechanism in place?

- Are monitoring thresholds and escalation protocols defined and assigned to an owner before the model goes live?

If any of these is a ‘no’, the model is not ready for deployment.

How TransOrg Analytics Approaches Model Risk Management Framework

At TransOrg Analytics, the model governance approach is focused on:

- Risk-based model classification

- Independent validation frameworks

- Automated monitoring and drift detection

- Explainability and transparency controls

- Audit-ready governance workflows

- AI governance aligned to RBI and global regulatory expectations

The goal is simple: to create trustworthy, explainable, and resilient AI systems that can scale responsibly.

Conclusion

Model risk management is a board-level discipline that determines whether an institution’s AI systems can be trusted, defended, and scaled. The regulatory bodies now expect the same rigor applied to credit and market risk to extend to every model making lending, fraud, and compliance decisions. For BFSI leaders building or refining their MRM framework, the guidelines are clear: tier by materiality, validate independently, document relentlessly, and monitor continuously.

If you are looking to build a model risk management framework that’s audit-ready and regulator-aligned, connect with our team to see how our AI governance approach helps BFSI institutions scale responsibly.

Key Takeaways

- Model risk management governs the full lifecycle of a model, including development, validation, deployment, monitoring, and retirement.

- AI model governance extends traditional MRM principles to ML and agentic AI systems making credit, fraud and underwriting decisions.

- RBI’s FREE-AI framework requires explainability, customer disclosure obligations, and grievance redressal mechanisms for AI-driven decisions.

- A defensible audit trail requires data lineage, model version tracking, decision checkpoints, and override logs.

- For responsible AI framework banking, model monitoring is an ongoing obligation with proper documentation and escalation protocols required through the entire model lifecycle.

FAQs

1. What is model risk management?

Model risk management is the board-approved governance framework that ensures every model used in lending, fraud detection, or compliance decisions is developed, validated, monitored, and retired through a documented, auditable process.

2. What is a model risk management framework?

A model risk management framework is the structured set of policies covering governance, model development, independent validation, and ongoing monitoring across a model’s entire lifecycle. RBI requires this framework to be board-approved and proportionate to each model’s materiality through risk tiering.

3. What does RBI require for model risk management in banking?

RBI’s model risk management guidelines require regulated entities to maintain a board-approved policy covering the full model lifecycle, conduct independent validation by a team not involved in development, and ensure outcomes are consistent, unbiased, explainable, and verifiable.

4. What is the RBI FREE-AI framework?

The RBI FREE-AI framework (Framework for Responsible and Ethical Enablement of AI) is RBI’s governance structure for AI in financial services, built on 7 Sutras and 26 recommendations. It extends model risk management, transparency, and cybersecurity requirements specifically to AI and machine learning systems.

5. What is model risk tiering?

Model risk tiering is the classification of models by materiality and potential impact, so governance effort is allocated proportionately. High-risk models like credit decisioning and fraud detection require full lifecycle oversight, while lower-risk tools receive lighter, proportionate controls.

6. What is the model validation process?

It is an independent assessment of a model’s conceptual soundness, data integrity, and predictive performance, conducted by a team not involved in its development. The RBI requires validation outcomes to be documented and reported to the Risk Management Committee of the Board.

7. What is required for explainable AI in banking?

Explainable AI in banking requires that model outputs be interpretable enough for a customer or auditor to understand the reasoning behind a decision. RBI’s FREE-AI framework specifically requires interpretation tools such as SHAP and LIME for AI-based decisioning systems.

8. What should a model governance checklist include?

A model governance checklist should confirm that a model has an assigned risk tier, has completed independent validation, has a documented explainability method, has an audit trail covering data lineage and overrides, and has monitoring thresholds defined before deployment.

9. How does model risk management apply to third-party or outsourced models?

Model risk management applies equally to outsourced or third-party models. Under RBI guidelines, the institution remains as accountable for these models as if they were developed internally, including ongoing validation and monitoring obligations.

10. What is an audit trail for AI-driven decisions?

An audit trail for AI-driven decisions is a documented record covering input data lineage, the model version used, the decision rationale or feature contribution, any human overrides, and the timestamp and approver of the decision required to make AI outputs defensible to regulators and customers.