Credit risk modeling refers to the process of using statistical and machine learning techniques to quantify the likelihood that a borrower will default and the expected loss if they do, which is measured through Loss Given Default (LGD) and Exposure at Default (EAD). Regulated industries such as banking, insurance and NBFCs use these models to replace manual underwriting and satisfy the capital and provisioning requirements imposed by Basel III and IFRS 9.

Introduction to Credit Risk Modelling

Every day, Indian banks and financial institutions process thousands of credit applications for home loans, personal loans, auto loans, corporate term facilities, etc. At that volume, manual underwriting is not just slow; it is impossible to do consistently and at speed.

The cost of getting it wrong is worse. Non-performing assets consume capital and lead to RBI supervisory action. Since credit risk is getting more complex, credit risk modeling is the structured and validated answer to this problem. It combines ML capabilities, regulatory frameworks and domain knowledge of credit to produce models that can be trusted and improved over time.

This guide covers everything about credit risk modelling, types of credit risk models, credit risk modeling techniques, and what monitoring looks like in practice.

What is Credit Risk Modeling?

Credit risk modelling is the use of statistical and ML techniques to quantify the probability a borrower will default (PD) and the expected financial impact if they do.

It is used by retail banks, NBFCs, corporate lenders, credit card companies and regulators whenever a credit decision needs to be made consistently, at speed and with documented logic per the regulatory frameworks.

Before credit risk assessment models became standard, lending decisions were made by credit officers using a combination of rule-of-thumb ratios, relationship judgment, and bureau scores. That approach worked at low volumes but was not scalable and did not satisfy modern regulatory requirements.

Core Concepts of Credit Risk Modeling

Credit risk modelling is not optional for regulated financial institutions. Basel III and IFRS 9 both require institutions to demonstrate their credit risk model validation, documentation, and fit for purpose before making any lending or capital decision and to avoid loan delinquency at any stage. The core concepts included in it are:

- Probability of Default (PD): The probability that a borrower will default within a given time duration (usually 12 months). For example: A person takes a ₹50 lakh home loan. There’s a 3% possibility that he may stop paying based on his credit history and income. Therefore PD = 3%

- Exposure at Default (EAD): The outstanding amount when the default occurs. For example: The person still owed the bank ₹40 lakh at the time of default . Therefore EAD = ₹40 lakh.

- Loss Given Default (LGD): It is the expected financial loss that the lender will lose if a default occurs. For example: The bank only gets ₹28 lakh by sale of the house. Banks lost ₹12 lakh out of ₹40 lakh. Thus, LGD = 30%

What Are Credit Risk Analysis Models?

Credit risk analysis models are different frameworks to assess a borrower’s creditworthiness based on his financial history, behavioral data, income, etc.

Which Factors Affect Credit Risk Modeling?

There are two types of factors that affect credit risk modelling:

- Borrower-Level Factors

- Credit history and bureau data: This includes payment history, delinquency records and utilisation from CIBIL, Experian, Equifax or TransUnion because they predict default probability.

- Income, Employment & Alternatives: Verified income, employment tenure, utility payments, rental history, mobile usage, and social signals since these are the primary repayment signals.

- Behavioral Signals: This includes transaction patterns, account activity, digital behavior etc., for customers who lack conventional bureau history.

- Collateral and Financial Statements: Collateral has a direct impact on the Loss Given Default. Also, financial statements are the main aspect of SME and corporate credit models.

- Macroeconomic Elements

- Economic Growth & GDP: Slow economic growth directly impacts income generation capacity. This increases the risk of defaults.

- Interest Rates: Any changes in interest rates can directly impact the cost of borrowing and repayment capacity.

- Regulatory Environment: Regulatory frameworks can help ensure financial stability and reduce credit risks.

Data Sources for Credit Risk Models

The quality of outputs from credit risk assessment models depends on the quality of data. The primary sources are:

Data quality is not a secondary option. Incomplete bureau coverage and internal data, or incorrect financial information, may lead to failure during credit risk model development. For enhanced credit risk modeling outcomes, agentic data management is something that you must not miss.

Types of Credit Risk Models

1- Credit Risk Scoring Model

- This model assigns a numerical score typically on a scale of 300-900 to predict the likelihood of default. This is mostly used for automated lending decisions such as personal loans, home loans, credit cards, and auto loans.

- This model in credit risk modeling is mainly implemented through a logistic regression model. It is best used when there are high volumes and standardised credit decisions that need to be automated without a manual underwriting process.

2- Credit Risk Assessment Model

- A credit risk assessment model evaluates a borrower’s overall creditworthiness, including financial ratio analysis, qualitative risk factors, and predictive scoring to set limits and determine credit grade.

- This model is used in corporate lending, SME finance, and project finance. It is best used when decisions involve significant human judgement along with model output.

3- Credit Risk Rating Model

- A credit risk rating model assigns a risk grade to borrowers, such as ‘very safe’ and ‘very risky’, to decide how much money to lend, what interest rate to charge and how much capital must banks keep aside as a safety net.

- RBI guidelines require that rating models be independently validated and tested to make sure they’re still accurate.

- It is best used when banks need one consistent model that drives both lending decisions and regulatory compliance.

4- Credit Risk Management Models

- Instead of looking at one loan at a time, this model checks the entire loan portfolio health of all the borrowers together to check the concentration risk, do stress testing and also calculate IFRS 9 Expected Credit Loss.

- This model works when CROs and CFOs need a portfolio-wide risk-view picture for capital planning, provisioning and regulatory reporting beyond individual credit risk models used by banks.

5- Predictive Models for Credit Risk

- While traditional models for credit risk modeling use simple rules like rejecting an application with a credit score below 650, predictive models use AI to analyze hundreds of signals together across spending patterns, repayment behavior, transaction history to predict who’s likely to default and when.

- The core challenge with ML models in credit risk is explainability. Regulators, the RBI in particular, require that credit decisions be explained at the individual level.

- SHAP (SHapley Additive explanations) and LIME are the standard post-hoc interpretability frameworks in credit risk modeling used to satisfy this requirement while retaining the accuracy benefits of ML.

How Credit Risk Models are used in Banks

A credit risk engine is a centralized platform that hosts, executes, and monitors all credit risk models, enabling real-time scoring, account management alerts, and regulatory reporting from a single governed environment.

These models are used for credit risk modeling at every stage of the credit lifecycle. The lifecycle looks like this:

- Origination: When a new loan application is received, the model analyzes and decides whether the applicant is eligible for a loan or not in real-time.

- Underwriting: For risky loans, the model gives a risk grade to banks and suggests the terms and conditions.

- Account Management: The model keeps a check on existing borrowers’ loan accounts to manage delinquency and send in timely reminders.

- Collections: The model ranks borrowers and analyzes who will pay back once the default occurs for effective collection strategies.

- Regulatory reporting: The PD, LGD, and EAD scores from the model are used to calculate how much capital the bank must keep aside per the guidelines and are reported timely.

- Portfolio Management: The model analyzes the bank’s entire loan portfolio to calculate the expected credit loss for IFRS 9 reporting.

Credit Risk Modeling Process

Credit risk modelling is a repeatable process. The outcomes are reviewed by the model risk committee, internal audit, and the regulator before any lending or capital decision is made.

The 5-step process is mentioned below:

- Problem Definition: The target variables (PD, LGD and EAD), the borrower population (retail, SME or corporate), the decision context (origination, account management or ECL) and the regulatory frameworks are defined before data collection.

- Data Collection, Cleaning and Quality Control : The internal data (such as transaction history, repayment records, and account behavior) is combined with external data (such as bureau data, financial statements, and macroeconomic indicators). Through exploratory data analysis (EDA), patterns, skewness and anomalies are classified to maintain the integrity of the model.

- Feature Engineering: Weight of Evidence (WoE) and Information Value (IV) calculations rank each candidate.

- Model Development and Default Probability Prediction: The refined features are used to train and improve models to achieve accurate predictions. This is done through strategies like cross-validation, L1 and L2 regularization, ensemble strategies, etc.

- Credit Risk Model Validation and Monitoring: ML model validation and audit are the final and the most important steps to ensure the long-term reliability of the models. This ensures that issues like bias and fairness are addressed for better long-term and efficient performance. The key metrics included in this stage are the Gini coefficient, AUC-ROC, KS statistic, Population Stability Index (PSI), and benchmarking. Once done, model monitoring for credit risk becomes an ongoing process to keep track of whether a deployed model continues to perform as expected or not.

What Are Credit Risk Modeling Techniques?

Credit risk modeling techniques are various ways to manage credit risk effectively. Different techniques are suited for different decision contexts, data environments, and regulatory contexts.

The common credit risk modelling techniques used throughout the process are:

Remember, in the credit risk modeling process, a credit risk model without structured monitoring is a regulatory liability because if the model drift goes undetected without PSI tracking, it can lead to mispriced risk or enforcement action.

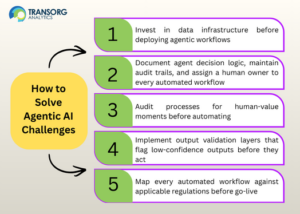

Common Challenges in Credit Risk Modeling

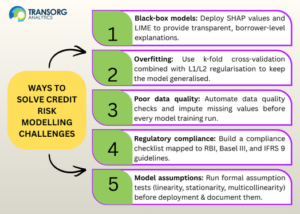

- Data Quality and Availability: Incomplete or inaccurate information is one of the most important reasons for failure for credit risk modelling. Poor quality of data leads to bad outcomes and thus affects a model’s performance.

- Explainability in ML models: Transparency is one of the important requirements in model deployment, as mentioned in the RBI’s FREE AI Framework report. The use of explainable AI methods such as SHAP values and LIME is important for interpreting decisions made by credit risk models used by banks to build trust.

- Overfitting: This is a particular risk that arises when ML models are trained on small datasets or when feature selection is not maintained.

- Regulatory Checklist: Different regulatory bodies have different requirements regarding ML model validation, documentation and development. This may lead to missing out on some guidelines due to timelines.

- Neglecting model assumptions: All the credit risk modeling techniques come with built-in assumptions about data and its relationships. These assumptions must be validated for efficient and reliable results.

Read the full case study here: TransOrg’s credit risk modeling approach to determine expected credit loss and distinguish it from incurred losses.

Conclusion

Credit risk modeling is not a single model or a technique. It is an integrated ecosystem, serving every stage of the credit lifecycle. Since regulatory institutions have major guidelines for financial institutions to establish trust and transparency in these models, on-time validation, documentation, and monitoring are non-negotiables.

Institutions that invest now in building the interpretability infrastructure around their ML models will be better positioned for the next phase of regulatory expectations. If you are looking to discuss credit risk model development and validation requirements, connect with us today!

Frequently Asked Questions

1- What is credit risk modeling?

Credit risk modeling is the use of statistical and machine learning techniques to quantify the probability that a borrower will default (PD) and the expected loss if they do (LGD, EAD). It is used by banks, NBFCs, and lenders to make credit decisions, set risk-based pricing, and meet Basel III and IFRS 9 regulatory requirements.

2- What are the types of credit risk models?

The main types of credit risk models are scoring models (automated retail decisions), assessment models (corporate and SME lending), rating models (Basel III capital adequacy), management models (portfolio-level ECL and stress testing), and predictive models using machine learning (early warning and lifetime ECL).

3- What is a credit risk assessment model?

A credit risk assessment model evaluates overall borrower creditworthiness by combining financial ratio analysis, qualitative risk factors, and predictive scoring to assign a credit grade and set exposure limits. It is used for complex, individually structured lending decisions where model output and credit analyst judgement are used together.

4- Which factors affect credit risk modeling?

The factors that affect credit risk modeling include borrower-level inputs such as credit history, income, collateral, and financial statements and macroeconomic inputs such as GDP growth and interest rates. The completeness and quality of data sources for credit risk models are the primary determinants of model accuracy.

5- What is a credit risk scoring model?

A credit risk scoring model assigns a numerical score to a borrower to predict their probability of default, which is the core tool for automating high-volume retail lending decisions. Credit risk scoring models are used by banks and lenders to approve, decline or refer decisions on personal loans, mortgages and credit cards in real time.

6- What is credit risk model validation?

Credit risk model validation is the independent assessment of a model’s soundness, data integrity, and predictive performance, which is required under Basel III and RBI Model Risk Management guidelines before a model can be used for capital calculations. Key metrics are the Gini coefficient, AUC-ROC, KS statistic, and Population Stability Index (PSI).

7- What is model monitoring for credit risk?

Model monitoring for credit risk is the ongoing process of tracking whether a deployed model continues to perform as expected. PSI monitors population drift; performance tracking identifies deviation between predicted and actual default rates; and RBI guidelines require documented escalation protocols and redevelopment alerts timely.

8- How are credit risk models used in banks?

Credit risk models used by banks operate at every stage of the credit lifecycle, including origination scoring, underwriting assessment, account management early warning, collections prioritization, and regulatory reporting. A credit risk engine is the centralized platform that executes all these models across the institution.

9- What is credit risk model development?

Credit risk model development is the end-to-end process of building a credit risk model from problem definition and data sourcing through WoE/IV feature engineering, model training, out-of-time validation, regulatory documentation, and deployment into a credit risk engine.

10- What are predictive models for credit risk?

Predictive models for credit risk use machine learning such as gradient boosting (XGBoost, LightGBM), random forests, and neural networks to forecast default with higher accuracy than traditional scorecards. Credit risk predictive modeling is applied to early warning systems and IFRS 9 lifetime ECL, where capturing non-linear borrower behavior is important.

11- What data sources are used in credit risk models?

The primary data sources for credit risk models are credit bureau data (CIBIL and Experian), internal bank transaction and repayment history, financial statements for corporate borrowers, and macroeconomic indicators. The alternative data sources also include utility payments, mobile usage, and rental history to identify thin-file customers without traditional bureau history.