Overview

If you are evaluating the role of agentic AI in lending, this blog breaks down exactly how AI acts autonomously in the credit lifecycle, where humans must stay in control, and what RBI-compliant AI deployment actually looks like. Know the six stages with clear AI vs. human boundaries for better decision-making.

Introduction

Agentic AI in lending involves a system that does not just predict credit risk but acts on it, such as initiating processes, triggering workflows, escalating edge cases and closing approval loops in the lending lifecycle autonomously at scale and in real time.

There is a lot of noise right now about agentic AI in lending, but for a lender, whether a bank, an NBFC, or a fintech, the real question is simple: can AI make the lending lifecycle faster, safer, auditable and profitable without creating new risks?

The answer is yes, but if you understand what kind of AI you are dealing with. Most banking and financial services institutions today have deployed predictive AI models that score, classify and flag. What is changing is the adoption of agentic AI in lending by financial institutions and alternative lenders across origination, KYC, credit underwriting, disbursement, portfolio monitoring, and collections. However, what they are still figuring out is how to design the right AI-human balance and what the regulatory bodies, such as the RBI in India and the FCA, the APRA or the EBA, globally expect.

This blog walks you through all six stages of the AI in NBFC lending and Indian banks’ credit underwriting process. It will take you through what AI does in each stage, what humans must still own, and why the distinction matters more in a global banking scenario.

The Role of Agentic AI in Lending Operations in Banks and NBFCs

Agentic AI is an AI system that:

- Interprets context from a variety of data sources, including documents, transaction history, market signals and bureau data.

- Makes decisions based on predefined rules and guidelines.

- Monitors outcomes and continuously learns for future outputs.

- Analyzes, takes action and recommends the next best possible solution

In lending, this matters because the lifecycle has six distinct stages, each with multiple decision points, and every delay or error compounds. For example, a 2-day lag in KYC costs you a customer, or a missed early warning signal costs you an NPA. Agentic AI in lending compresses those decision cycles from days to minutes, but only when it is deployed with clear guardrails and the right human checkpoints.

The TransOrg’s Human-AI Accountability Principle

At TransOrg, we apply a simple framework for responsible deployment of agentic AI in lending:

Detection → AI | Decision Support → AI | Judgment → Human | Accountability → Always Human

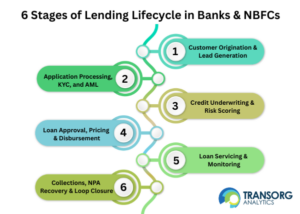

6 Stages of Lending Lifecycle & Role of Human Control

Since agentic AI in lending is becoming more adoptable and credit risk is getting more complex, it’s important to know what AI does at each stage and where humans stay in control of the lending lifecycle.

Stage 1 – Customer Origination and Lead Generation

The customer origination and lead generation are the processes of identifying, qualifying, and engaging prospective borrowers before a loan application is submitted. In this stage, this is where agentic AI makes an impact:

- AI-driven loan origination starts before a customer even applies for it. Propensity models can flag customers who are likely to need a loan in the next 60-90 days and score their creditworthiness without needing any documentation upfront.

- Real-time lead de-duplication across CRM systems ensures your sales teams are not reaching out to the same prospect twice.

- Channel ROI attribution lending helps optimize the cost of acquiring loans by analyzing which channels, such as email, WhatsApp, SMS, social media, etc., are the most effective.

Where humans stay in control in agentic AI in lending:

In this stage, DSA and distribution partner decisions are still relationship calls. Customer financial counseling, which is a regulatory requirement in several loan categories, must stay human-led even in the age of agentic AI in lending.

Stage 2 — Application Processing, KYC, and AML

Application processing, Know Your Customer (KYC) stage, involves verifying borrower identity, validating documents, and screening applicants within the defined parameters before credit assessment begins.

Manual KYC, physical document verification, and back-and-forth between branches and applicants added days or weeks to what should be a same-day process. Decisioning through Agentic AI changes this scenario completely such as:

- Modern OCR and Intelligent Document Processing platforms extract data from PAN cards, Aadhaar, and passports with up to 98% accuracy.

- ITR parsing and Form 16 analysis compute net income from structured government documents.

- On identity verification, video KYC face liveliness, Aadhaar e-KYC and CIBIL, Equifax and Experian confirm who the borrower is in real time without a branch visit.

- Synthetic identity detection is being done through anomaly scoring to flag unusual combinations that no human reviewer would catch at volume.

- Politically exposed person and sanctions list screening runs in parallel, consistent with PMLA obligations under Indian anti-money laundering law.

Where humans stay in control in agentic AI in lending:

First-time borrowers cannot be reliably scored by agentic AI in lending decisions for banks and financial services institutions alone and require judgement-based decisions. HNI and priority segment borrowers often expect and receive a relationship banker override. And PMLA obligations ultimately require human compliance sign-off.

Stage 3 – Credit Underwriting and Risk Scoring

Credit Underwriting is the process of evaluating a borrower’s creditworthiness using bureau data, financial records, behavioral signals and risk-scoring models to determine loan eligibility, interest rate and closure terms.

Though AI is making a major impact in credit underwriting, and it is also where the debate on AI vs human in loan underwriting is intense. This is because the cost of getting it wrong is highest here.

- Application scorecards combine bureau data, behavioral signals and other data sources, giving a more clearer picture than traditional CIBIL score-based decision-making.

- Loan-specific models built separately for Personal, Home, Business, Gold, and MSME loans help in better risk profile segmenting.

- For those in the thin-file and NTC groups, GST transaction flows and UPI payment history are becoming more reliable indicators of income and repayment ability in the age of agentic AI in lending.

- Loan delinquency forecasting through time series models and vintage analysis for DPD bucket prediction is also where AI for NPA prediction is showing results.

Where humans stay in control in agentic AI in lending:

In this context the simple question that comes up is ‘can AI replace credit officers in India?’ The answer is no. This is because while AI can handle the majority of tasks to ensure RBI compliant AI credit decisions within defined rules and parameters, it struggles with edge cases such as CIBIL score exceptions, HNI relationship banking, MSME founder profiles, new-to-credit profiles, and physical gold verification for gold loans.

Stage 4 – Loan Approval, Pricing, and Disbursement

Loan approval and disbursement is the process of converting underwriting decisions into sanctioned loans to the chosen borrowers through pricing, approval workflows, and fund release mechanisms.

Once the credit is approved, speed matters. Every hour of delay between approval and disbursement may lead to a drop-off. Agentic AI in lending compresses approval to disbursal cycle through AI workflow automation that can move from approval to disbursal in hours instead of days.

- Through risk-based pricing engines, financial institutions are able to build a segment-specific score-rate matrix based on each borrower’s risk profile instead of applying a flat interest rate by product.

- Pre-approved loan offer generation automatically identifies opportunities for top-up loans or cross-sell products based on repayment histories.

- Risk-based pricing combined with Fixed Obligation-to-Income Ratio (FOIR) constraints and LTV parameters ensures the bank’s net interest margin is protected across the loan book.

Where humans stay in control in agentic AI in lending:

When it comes to business loans that exceed a certain limit, usually around 50 lakh INR, a credit committee’s approval is a must. For large amounts outside defined parameters of agentic AI in lending systems, as an added layer of security, approval of two senior members is needed.

Stage 5 – Loan Servicing, Monitoring, and Early Warning

Loan servicing and monitoring involve continuously tracking borrower behavior, portfolio health, and emerging risk indicators throughout the tenure of the loan. This includes steps like:

- Portfolio risk re-scoring and delinquency probability scores are refreshed in line with the RBI’s FREE AI framework principles (Fairness, Accountability, Transparency, Ethics, and Responsible AI Governance).

- Vintage analysis at the cohort level provides NPA forecasting by loan type, giving the risk team a forward-looking view of which customers are likely to default.

Where humans stay in control in agentic AI in lending:

For likely-to-default accounts, relationship manager outreach is a human-lead intervention in the era of agentic AI in lending. Regulatory reporting, including Special Mention Account (SMA) classification under RBI guidelines, needs compliance officer review. Not only this, board-level NPA provision approval is a governance requirement

Stage 6 – Collections, NPA Recovery and Loop Closure

The collections and recovery stage involves identifying delinquent accounts, engaging borrowers, maximizing recoveries, and resolving non-performing assets while maintaining regulatory compliance.

This is the stage where agentic AI in lending has the most immediate ROI, because the cost of inefficient collections is clearly visible in every P&L.

- AI-automated SMS, WhatsApp, and IVR nudges reach borrowers at the right time when each individual borrower is likely to respond.

- Self-cure propensity models identify which borrowers are likely to self-correct without any intervention, allowing collections teams to focus on accounts that actually need attention.

- Agentic AI helps in better customer segmentation for implementing better collection strategies.

- Digital payment links and settlement offer calculators give borrowers a convenient way to resolution.

- AI-transcribed collection calls with sentiment scoring identify calls where the borrower is distressed, cooperative or hostile to route them accordingly.

Where humans stay in control in agentic AI in lending:

In the last stage, humans determine and approve the One-Time Settlements (OTS) parameters to recover principal amounts. In cases of Insolvency Bankruptcy Code filings, and loan closure, human intervention is a must in further proceedings.

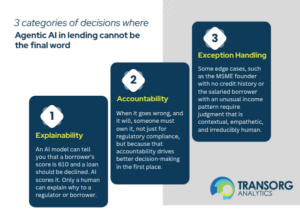

Why the Human-AI Balance is Non-Negotiable in Indian Banking

The RBI has been thoughtful about agentic AI in lending. Its guidelines on digital lending, data management and governance, and credit underwriting all point to the same principle: AI can support the decision, but humans must own the accountability. This is sound risk management and governance.

There are three categories of decisions where AI in NBFC lending India simply cannot be the final word:

Therefore, the right approach to implementing agentic AI in lending is not AI replacing humans but AI doing what it is best at, like processing data at scale, identifying patterns, and automating high-volume decisions within defined parameters while humans focus on judgment, exceptions, and accountability.

Measurable Impact of Agentic AI in Lending Stages at Banks and NBFCs

The major benefits of agentic AI in lending across underwriting, collections, KYC processing, etc., that financial institutions are seeing include the following:

-

Faster Loan Processing and Decisioning

Industry research indicates that AI-driven underwriting and lending automation can reduce loan processing time by up to 50-75% and also 6-8 days, down from the 12-15 day average approval cycle.

-

Stronger Portfolio Monitoring and Early Risk Detection

Most banks find out a loan is going bad when the customer misses a payment. Enhanced credit risk modeling techniques and an Early Warning System (EWS) banking powered by agentic AI in lending operations find out 60 to 90 days before that happens.

-

Better Underwriting Productivity

Credit teams spend a significant time on gathering, validating and reviewing information rather than making decisions. Industry research shows that there has been approximately a 25% reduction in default rates through AI underwriting compared to traditional underwriting methods.

-

Improved KYC and Compliance Efficiency

Know Your Customer (KYC) and Anti-Money Laundering (AML) processes remain among the most resource-intensive functions in banking. According to McKinsey, banks commonly allocate 10–15% of their workforce to KYC and AML activities alone. Agentic AI helps automate onboarding, verification, screening, and compliance workflows, creating significant efficiency gains.

-

The Competitive Advantage

Agentic AI in lending operations with human control at required checkpoints ensures faster, scalable and more compliant decisions in an increasingly competitive market.

Conclusion

Agentic AI in lending does not replace credit judgement; instead, it protects it by handling the volume, the speed, and the pattern recognition with humans in the loop for accountability. The next five years in Indian lending through banks and NBFCs will be defined by which financial institution has built the right human-AI balance from the start.

TransOrg Analytics works with global banks and financial institutions to design and implement agentic AI solutions for lending. If you are evaluating AI in credit underwriting, collections, or early warning system implementation, connect with our team today.

FAQs – Agentic AI in Lending

1- What is agentic AI in banking, and how is it different from traditional AI?

Traditional AI in banking tells you what is likely to happen. Agentic AI in banking acts on those predictions by triggering workflows, making decisions within defined parameters, and closing the loop between insight and action. In lending, this means an agentic system does not just score a loan application; it routes it, enriches it with bureau data, initiates KYC verification, and generates a sanction letter, all without human intervention at each step.

2- How do banks use agentic AI in lending, for collections and NPA recovery?

Agentic AI in lending optimizes the timing, channel, and tone of borrower outreach based on individual behavioral profiles. It identifies self-cure accounts, prioritizes high-recovery accounts for agent attention, assists in settlement offer modeling, and monitors call quality and agent performance in real time. This reduces cost-to-collect while improving recovery rates, particularly in the early-bucket delinquency population.

3- What is meant by Early Warning System (EWS) banking?

An EWS continuously monitors a portfolio of loans for signals that predict future default through declining transaction volumes, bureau deterioration, increased credit utilization elsewhere, payment irregularity patterns, and external stress signals. By flagging accounts 60 to 90 days before they become NPA, the bank can intervene proactively through relationship outreach, restructuring conversations, or increased monitoring before the loan formally deteriorates.

4- Can agentic AI fully automate lead generation for a bank?

No. AI can score, prioritize, and route leads with high accuracy, but partnership and DSA relationship decisions, campaign strategy, and geographic expansion into new markets require human judgment. Fair lending compliance with regulatory bodies’ guidelines also needs human ethical review.

5- How do Indian banks use AI for KYC and AML compliance?

Banks use AI to automate document extraction, identity verification, and screening against PEP and sanctions lists in real time. AI can process hundreds of applications simultaneously at a fraction of the manual cost. However, PMLA compliance sign-off, decisions on thin-file or first-time borrower applications, and overrides on bureau edge cases still require human approval under RBI guidelines.

6- Can AI replace credit officers in India?

No. AI can automate a significant proportion of straightforward underwriting decisions within well-defined score bands, but boundary cases, MSME and HNI segments, policy exceptions, and RBI compliance requirements all mandate human involvement. The RBI’s guidelines on digital lending explicitly require human accountability in the credit decision chain.

7- What is risk-based pricing in loan disbursement?

Risk-based pricing links each borrower’s interest rate directly to their measured credit risk. Rather than offering the same rate to all customers in a product category, banks use a Score-Rate matrix that adjusts the rate based on CIBIL score, FOIR, LTV, loan tenor, and segment-specific risk factors. This protects NIM at the portfolio level while theoretically offering better rates to lower-risk borrowers.

8- What human approvals are required by RBI for agentic AI in lending?

RBI guidelines require human accountability at multiple points: PMLA compliance sign-off in KYC, credit committee approval for business loans above defined thresholds, four-eye disbursement checks, SMA classification, restructuring decisions, NPA provision approval, and all legal enforcement actions under SARFAESI and DRT. The overarching principle is that AI can support and automate, but humans must own consequential decisions and their regulatory accountability.